|

FEC offers managed ownership with significant income plus maximum deductions! Additional advantages for ownership verses producing land or commercial property plus significant tax potential savings see below or go to advantaged.

Diversified Family Asset Estate Planning - Eliminate Hassles - Management & Tax Work - Keep Best Assets - Exchange to Better Asset |

Referral Work Direct with Project Manager

2020 Barron-Keck Real Estate Redevelopment Project (Six oil & gas wells in place rehab income project)

Goal: High Income*High Deductible*Longevity Real Estate

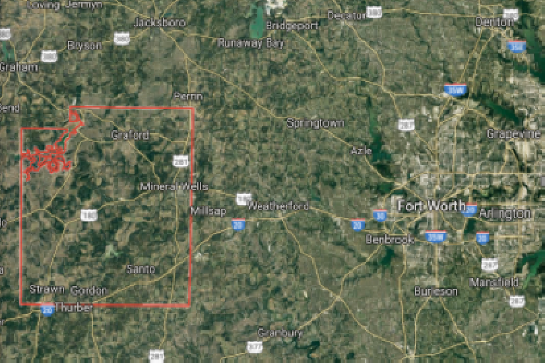

Palo Pinto County Texas Approximately 40 Miles West of Dallas-Ft. Worth, TX

| 2020 Barron-Keck Rehab & Development

Project

|

|

2020 Barron-Keck Rehab & Development

Project

|

$25,000 minimum; Income Rehab Hold or Divest Project $825,000; $250k Start up

More detail below; ask for more detail of rehab project goals here

For Property Purchase, Work Direct with Barron Keck Project Operator

Recorded Ownership Assignment

Oil & Gas Ownership Guide (45 Pages PDF) To visit with Manager-Operator: Confidentiality-Non Disclosure Agreement

|

Significant benefits for FEC income rehab-rework-redevelopment properties Reduce Debt while Maintaining Income Goals Rehabilitated - reworked - updated - redeveloped & modernized for efficient income & accelerated gain properties 1031FEC model strong points reduce owner risk and management. Comprehensive management with active participation tax advantages §469. Working interest and passive investment: If one owns a working interest in any oil or gas property, either directly or through an entity that doesn't limit the taxpayer's liability with respect to the interest, it is non-passive activity, regardless of the taxpayer's participation. Real estate local recorded legal description assignment plus Texas Railroad Commission Properties can have CPA and/or Operator experienced management in place Improvement production income goal 15%-25% simple annual (potential larger returns) Can be ong term asset with income for family generations if preferred. can sell as wish or be a long term hold asset. Qualifies for step up basis for generational asset hold. Consistent production harvest flow goal current on going production 24/7 365 days a year Income has 15%+ depletion allowance or potential principal reduction tax advantage Pay No or Less Tax - most significant tax deduction (100%, 75%-90% first year) in USA- most income classes; Your tax advisor, CPA to confirm your individual tax status; Invite your CPA. CPA inquiries invited. Financial & Production Reports; Quarterly income, production and rehab reports Individual Retirement Account (IRA)/Roth IRA and Family Office qualified - Increase Family wealth Some projects shorter term ownership (three-four year goal) with asset appreciation profit; integrate Estate & Financial Plans Increase returns - reduce current and future income taxes while in rehab-redevelopment hold-ownership Tax deferral - defer or eliminate capital gain and recapture of depreciation tax; See example at 1LessTax-Page3 Internal Revenue Service Code (IRC) §1031, §1033, §721, §179 & §469 qualified Pay No or Less Tax - can replace a 1031exchange without IRS time limit, debt or $ limits; gain-recapture significance. Create cash for new depreciation. Keep basis $ verses 1031 Exchange; Can cover Gain and/or Recapture Proceeds with purchase amount without basis or debt Pay No or Less Tax - can roll replacement gain into a 1031 exchange or replace with new rehab-rework project; save lowering tax bracket Real Estate owner & CPA determine entity advantage after initial in year ownership (LLC, joint venture (JV) or other) $25k to $100K minimum field real estate rehab projects entry can be available at times. Other projects: $1M minimum - Current field rehab project $6M; Hold for three-four years then divest; please inquire. Other field projects to $50M+ with significant ownership required for most properties Projects generally have goal of less than 10 qualified and familiar owners vested in one real estate field Purchase qualification of $300k annual income or less residence value net worth total $1M Financial advisors recommend purchase maximum of 30% of net worth unless experienced with asset Please Note: Projects can close anytime with maximum participants, members and/or joint venture associates. Recommend projects owner have experienced personal CPA/tax advisor for maximum tax advantages. Go To Page PM2 General 1Lesstax 14 Options Energy Rehab & Other RE Types Sale-Lease Back |

Vision: Assist owner to maintain and improve valuation of assets with proper tax control. Mission: Use industry specific professional tax advisors to relieve owner tax burden coordinating with owner's financial and estate plan goals using deductible income property . What we do A Mergers and Acquisitions (M&A) background and experience in agriculture and energy allow FEC and Ken Wheeler Jr. to be familiar with some tax advantages many tax professionals may not encounter. We consistently valuate the most attractive and advantaged real estate income properties for your approval. Properties currently available - several properties presently for acquisition or joint venture Small to Larger properties available - Off-market and private property inventory varies - other states available Inquiries invited for these private income real estate opportunities Confidentiality-Non Disclosure Agreement

|

Why FEC ?

1031FEC is experienced with years in diversified property income production. FEC offers absolute comprehensive managers for

real estate owners desiring significant income and tax advantages while maintaining a more passive management role because of

other business commitments, retirement goals or asset diversification.

FEC is a property manager intermediary of Financial Exchange Coterie & K. B. Wheeler Jr.

Inquire about

Sale - Leaseback,

Exchanges

and

§179 with Bonus

Tax Advantage for

§1245

inherent properties

For Current or Future Projects Contact us

Stop Beneficiary Conflict www.LegacyChange.com for Economical - Simple Estate Plan

For a informational meeting online or in person contact Ken

We recommend consultation with your personal and business Tax Advisors.